When you’re selling a house, a “good offer” isn’t always the one with the highest price. The best offer is usually the one that gives you the highest net proceeds with the lowest risk of falling apart — and a closing plan that fits your timeline.

Price matters, but so do the terms: contingencies, financing strength, earnest money, and how quickly (and smoothly) the buyer can close. A strong listing agent can help you compare offers using a net sheet and negotiate for better terms — often improving your bottom line even when the headline price stays the same.

If you're looking for a realtor, we can help you connect with top agents in your area. These agents are skilled negotiators and offer full service for half the typical listing fee (1.5% vs. 3%), potentially saving you thousands on your home sale.

1. Higher net proceeds

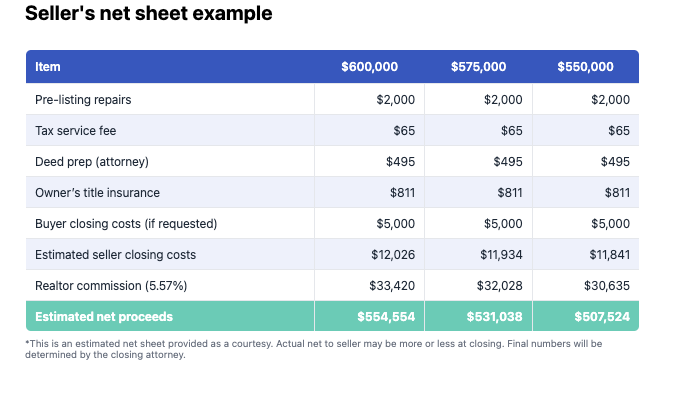

Net proceeds (how much money you'll walk away with from your sale) will likely be your main consideration when reviewing offers. Your net proceeds aren't the same as the sale price a buyer offers; they're the sale price minus closing costs, seller credits, and any other expenses.

Your real estate agent will use a seller’s net sheet to help you understand how much money you’ll actually pocket based on each buyer’s offer. You can also use a home sale calculator to learn how to calculate your net proceeds.

For example, you could get two offers with the same sale price of $800,000. The first offer asks you to cover $20,000 in closing costs, a home warranty, and the termite inspection. The second offer doesn't ask you to cover these additional costs.

Even though the sale price is the same, the second offer is the better deal since it will leave you with higher net proceeds.

2. Fewer contingencies

A major component of any offer is the set of real estate contingencies — the conditions that allow the buyer to back out (or renegotiate) if something goes wrong.

In general, fewer contingencies can mean a stronger offer for the seller, because there are fewer ways for the deal to derail. But it’s not always realistic — and it’s not always smart — to accept an offer with no protections at all.

Instead, look for contingencies that are reasonable and clearly defined, such as:

- A shorter inspection period (so you’re not stuck in limbo)

- Clear limits on repair requests (for example, the buyer won’t ask for minor fixes)

- A strong plan for appraisal risk (such as the buyer having funds to cover an appraisal gap, if needed)

Cash offers can also be attractive because they remove the financing contingency entirely — meaning there’s no lender approval step that can delay or derail closing.

3. Strong financing package

If the buyer isn’t paying cash, the next biggest question is: How likely is this buyer to get to closing on time?

A strong financed offer usually includes:

- A true mortgage pre-approval (not just a pre-qualification), ideally with the lender’s contact info

- Proof of funds showing the buyer can cover their down payment and closing costs (and any appraisal gap they’re offering to cover)

- Clean paperwork and realistic deadlines that match lender timelines

Conventional loans are often viewed as straightforward, but FHA, VA, and USDA loans can still be solid — especially with a well-qualified buyer and a lender who closes reliably. The key is whether the loan type and the property are a good match, and whether the timeline is realistic.

Your listing agent can usually spot red flags fast by reviewing the pre-approval details and calling the lender.

4. Higher earnest money deposit

Earnest money is the buyer’s good-faith deposit — and it signals how committed they are to the purchase.

In many markets, earnest money often falls around 1–3% of the purchase price, but norms vary widely by location and competition.

A higher earnest money deposit can strengthen an offer because the buyer has more “skin in the game.” All else equal, a buyer putting down a meaningful deposit may be less likely to walk away without a valid reason.

That said, earnest money only protects you if the contract terms allow you to keep it when the buyer breaches — which is one reason it’s helpful to lean on an experienced agent (and, in some states, an attorney) when evaluating offers.

What is considered a high earnest money deposit will vary depending on local market conditions. When you choose a realtor for selling your house, they should be able to provide guidance about what standard earnest money deposits look like in your area.

5. Standard or shorter closing timeline

Closing timelines matter because time introduces risk: the longer a deal stays open, the more chances there are for financing, inspection, or life circumstances to change.

A faster close can be appealing — but the best timeline is the one that fits your plan. Some sellers want speed so they can move on quickly, while others prefer flexibility (for example, extra time to find a replacement home or a short rent-back after closing).

A loan officer on Reddit shares, “Faster closing = less chance of something going wrong. In my experience, things go bad when stagnant. Also, getting your money earlier can be important if the seller needs it to buy a new house, pay off a spouse in a divorce, etc.”

As you compare offers, consider:

- Is the proposed close date realistic for the buyer’s financing?

- Does the timeline reduce uncertainty — or create it?

- Does it match what you actually need?

A good agent can often negotiate timelines and possession terms to make a strong offer even stronger.

FAQ

Is 90% of the asking price a good offer?

In a buyer’s market where homes take longer to sell, a 90% offer can be attractive. But in a seller’s market where homes are in high demand, an offer that's 10% below asking will likely be too low. Learn more about how to sell a house, including negotiating offers.

What might make an offer weak?

An offer may be weak if it's well under the asking price or if it has too many contingencies. Offers that are dependent on financing approval are also typically weaker than all-cash offers. However, what’s considered a weak offer varies by market, so you’ll want to find a real estate agent for local guidance.

Who typically presents an offer to the seller?

Offers are typically presented to the seller by the listing agent. If the buyer has an agent, the buyer’s agent will give the offer to the listing agent, who then shows it to the seller. Both agents will negotiate on behalf of their clients. Learn more about how to negotiate a home sale.

Related reading